The June “flash” PMI® survey data provides an early look at the state of the Eurozone economy after the European Central Bank cut interest rates for the first time in five years. The survey shows that the pace of economic growth unexpectedly slowed, contrary to consensus expectations of a further acceleration in growth. Manufacturing in particular weakened, with the rate of deterioration accelerating sharply. At the same time, however, price pressures have slowed further, falling from historical comparisons to levels consistent with the ECB's inflation target.

Here are five key takeaways from the preliminary June PMI data:

1. Economic growth declined in June

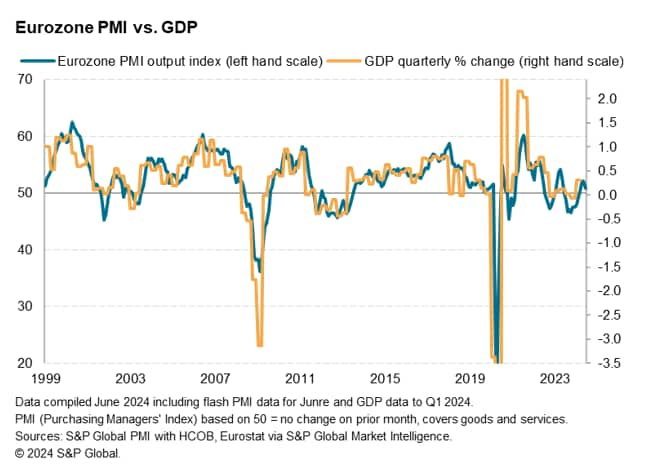

The seasonally adjusted HCOB flash euro zone composite PMI output index, compiled by S&P Global based on about 85% of normal survey responses, fell to 50.8 in June from 52.2 in May. Economists had expected a rise to 52.5.

While it suggests output has grown for a fourth consecutive month after a nine-month period of decline, the latest reading is the lowest in three months and points to euro area GDP languishing with quarterly growth of just over 0.1% (according to a simple OLS regression model based only on previous PMI and GDP data). For the second quarter as a whole, the PMI average of 51.6 suggests GDP would rise by 0.2%.

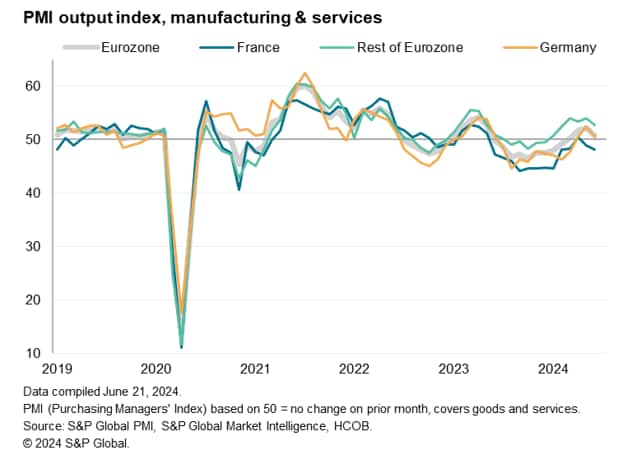

The worsening euro area growth trend was led by France, where output fell for a second consecutive month, the sharpest decline in five months. Companies reported that the deterioration was partly linked to increased uncertainty and sluggish spending following the sudden announcement of parliamentary elections. France's flash composite PMI pointed to stagnant GDP in June and a mere 0.1% expansion over the second quarter as a whole.

However, growth in Germany has also slowed significantly from a 12-month high in May, although it still recorded a third consecutive month of growth after nine months of declines.Still, the flash composite PMI reading for June showed no GDP growth for the month and quarter, and, like France, showed the economy growing at just a 0.1% pace for the quarter.

But outside of France and Germany, the picture is brighter: The rest of the euro zone reported a sixth consecutive month of output growth in June, although growth lost momentum to a four-month low and was still above the long-term average.

2. Declining manufacturing production

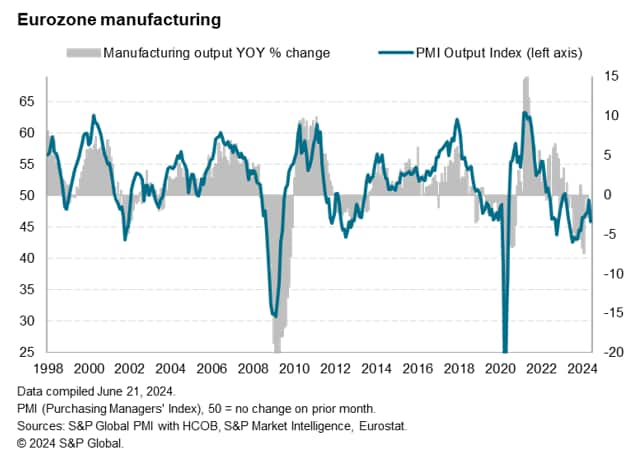

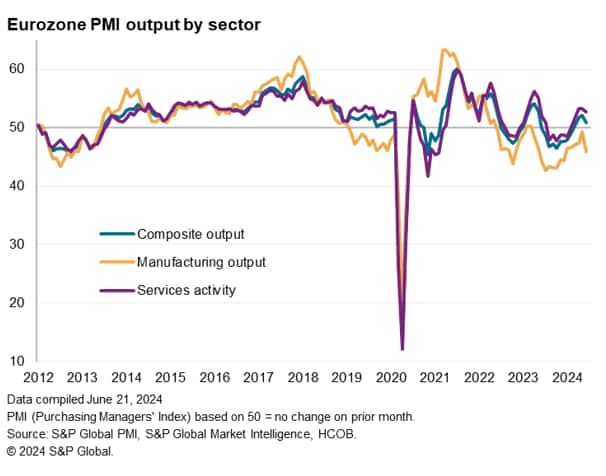

Broken down by sector, the deterioration in the euro area as a whole in June was driven by a sharp drop in manufacturing output. Factory output, which had been broadly stable in May, fell by the most in six months and the 15th consecutive month of sector decline. Output declines accelerated in France and Germany, reaching their highest levels in five and three months respectively, while output in the rest of the euro area fell again, marking the biggest drop since December.

Adding to the manufacturing slump is a sharp decline in new orders, which fell for the 26th straight month in June, reversing a gradual trend of recent months, as demand indicators worsened in France, Germany and other euro zone countries.

3. Expanding services sector offsets factory slump

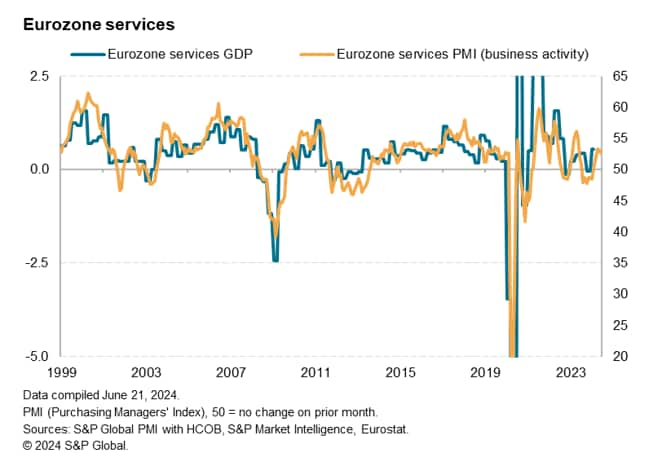

Meanwhile, the services sector maintained its expansion for a fifth consecutive month, although growth slowed to its slowest since March. The slowdown mainly reflected a decline in business activity in France, which is often linked to political uncertainty (though a small decline was also recorded in May). Growth in Germany and the euro area as a whole also lost some momentum, but these expansions remained encouragingly strong by the survey's recent standards.

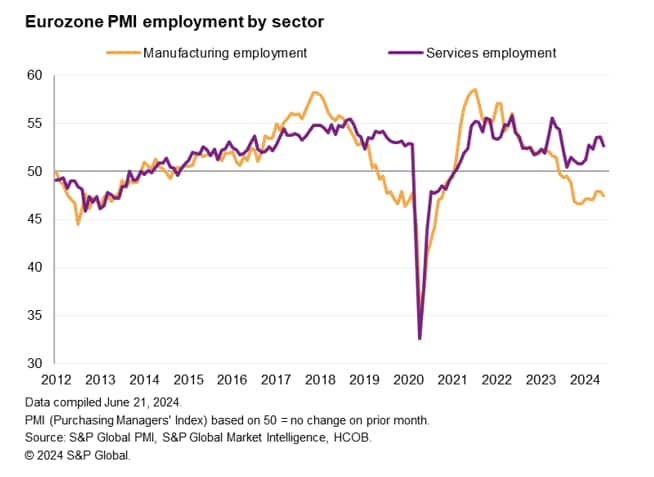

4. Uncertainty will hurt employment

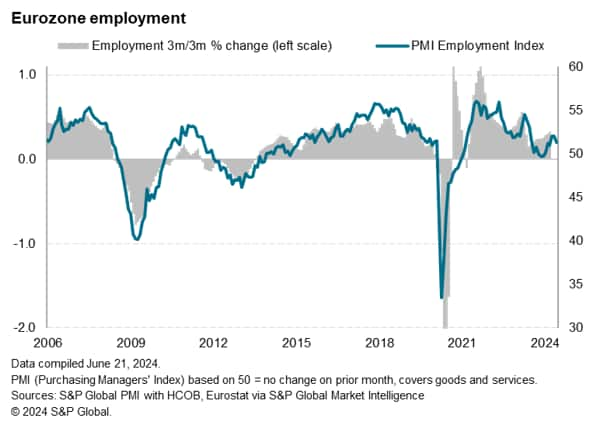

Across the euro zone, employment rose for a sixth consecutive month in June after two months of small declines at the end of last year, but the latest increase was the smallest on record in three months. In Germany, employment fell slightly for the first time in three months following manufacturing layoffs, while in France and other euro zone countries, employment growth fell to three- and four-month lows respectively, driven again by manufacturing job cuts.

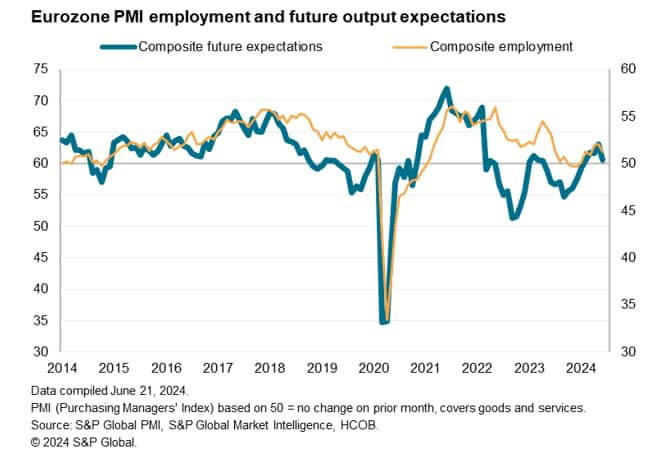

Hiring took a hit as businesses became less optimistic about their prospects for the year ahead, with production expectations across the euro zone falling in June to the lowest since February.

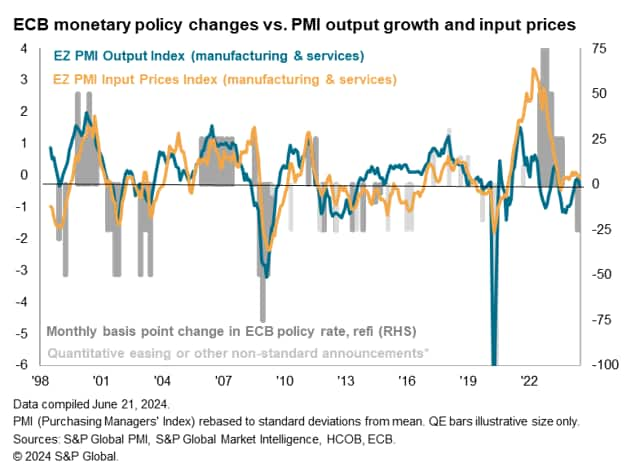

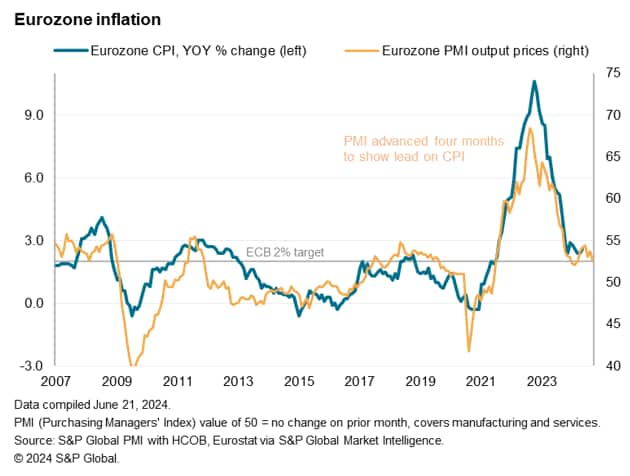

5. Price growth will slow

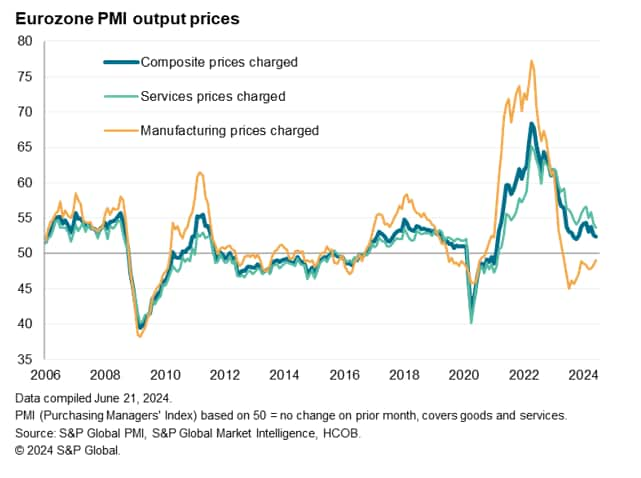

Average prices for goods and services across the euro zone rose to an eight-month low in June and the lowest level since inflation accelerated in early 2021. Based on historical comparisons, the fall has brought the index back to a level roughly in line with the ECB's 2% inflation target.

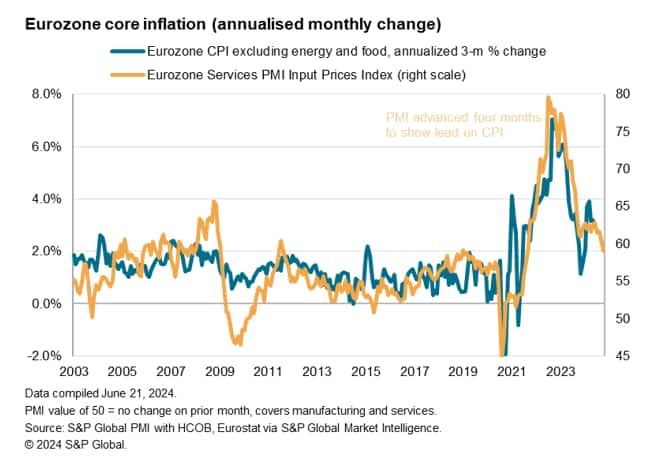

Of particular note, input costs in the services sector, which are highly sensitive to wage growth, rose at the slowest rate since April 2021, signalling a slowdown in core inflation (which also fell to target).

However, manufacturing disinflationary trends eased further in June, while lower input costs in the services sector led to the weakest rate of increase in selling prices of services recorded in the survey since May 2021. Factory input costs rose for the first time in 16 months in June, resulting in the smallest rate of decline in manufacturing selling prices in over a year. If this trend persists, it could put fresh upward pressure on inflation in the coming months.

Within the euro area, price growth was particularly weak in France, where the average price of goods and services rose slightly in June, the slowest increase since prices began to rise in March 2021. Services prices in particular rose slightly in France. In Germany, price growth rose slightly, but the rate was the slowest in three years and only slightly above the pre-pandemic decade average. Meanwhile, euro area inflation slowed to a six-month low.

Please see the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Phone: +44 207 260 2329

chriswilliamson@spglobal.com

© 2024, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers Index™ (PMI®) data is compiled by S&P Global for more than 40 economies around the world. The monthly data comes from a survey of senior executives from private companies and is available only via subscription. The PMI dataset includes headline figures that indicate the overall health of the economy and sub-indices that provide insights into other key economic factors, including GDP, inflation, exports, capacity utilization, employment and inventories. PMI data is used by finance and corporate professionals to better understand the direction of the economy and markets and to uncover opportunities.

PMI data details

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, a division of S&P Global.