Preliminary PMI survey data shows business activity in the euro zone fell even more sharply in December, with production falling at the fastest pace in 11 years in the fourth quarter, excluding only the pandemic months of early 2020. concluded. Weakness was recorded again in both manufacturing and services.

It was the second straight month of job cuts as companies reduced operating capacity due to a worsening order book and a persistently poor outlook for next year. Factories also reduced raw material inventories by rates not seen since 2009.

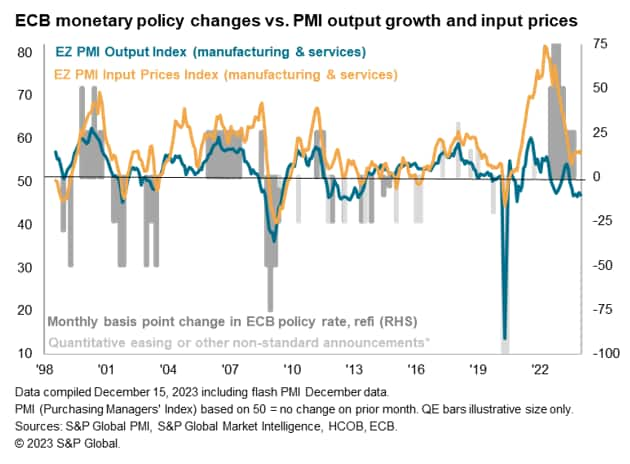

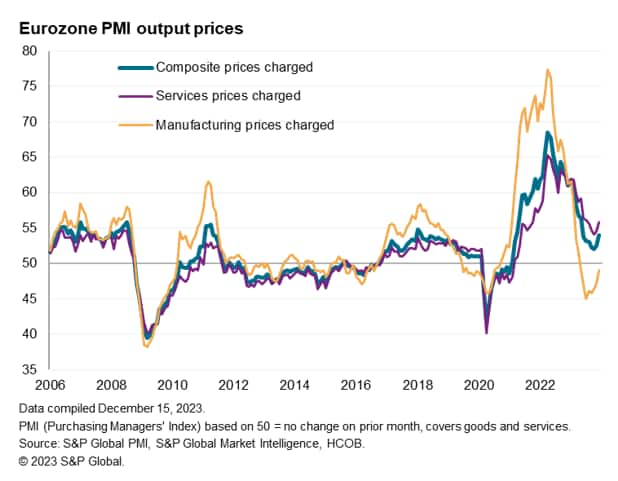

Inflation signals were mixed. While input cost inflation slowed, sales price inflation accelerated, with the latter still notably high by historical standards.

signal of recession

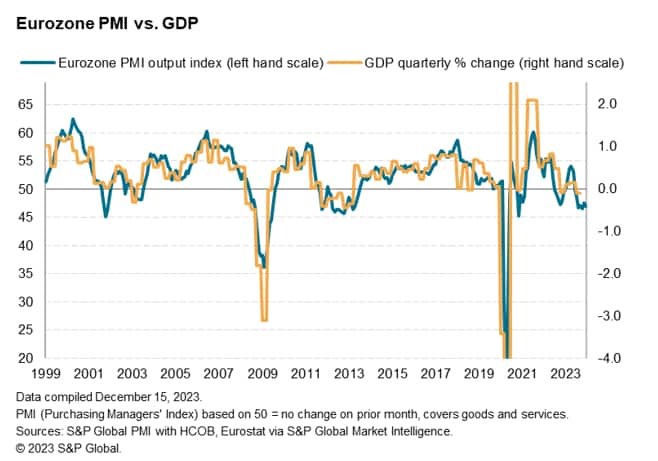

The seasonally adjusted HCOB Flash Eurozone Composite PMI Production Index, compiled by S&P Global based on approximately 85% of regular survey responses, hit 47.0 in December, down from 47.6 in November and across the eurozone. It marked the seventh consecutive month of decline in business activity. . The weak figure would round off the steepest average quarterly decline in activity since the fourth quarter of 2012 recorded in the survey, excluding the early lockdown months of the pandemic.

PMI data broadly indicates that GDP in the fourth quarter will decline by 0.2% to 0.3% from the previous quarter. Following negative growth of 0.1% in the third quarter, negative growth in the fourth quarter will likely push the euro area into a technical recession.

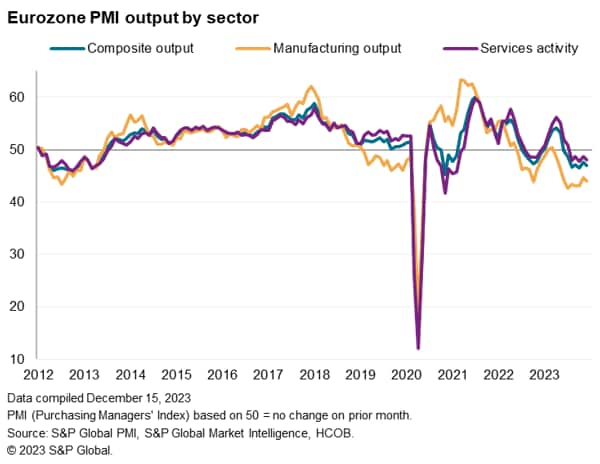

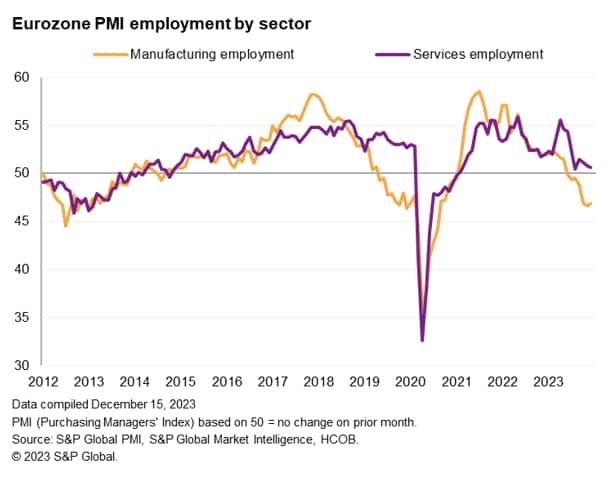

Manufacturing continued to lead the economic downturn, and service sector production also declined sharply. Manufacturing production fell for the ninth consecutive month, with the rate of decline reaccelerating slightly from the slowdown seen in November, but still not as severe as in the four months through October. Meanwhile, service activity fell for the fifth consecutive month, and the pace of decline picked up slightly again, marking the third-largest drop since the lockdown in early 2021.

Deterioration of demand environment

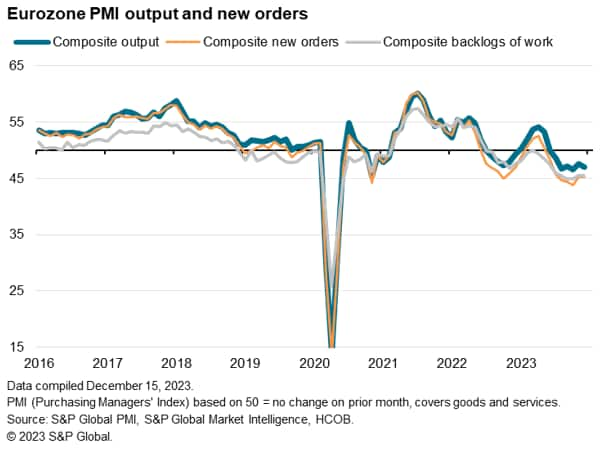

The decline in overall business activity again reflected a deterioration in order intake. The inflow of new orders declined for the seventh consecutive month, with the rate of decline unchanged from the steep pace seen in November (though not as steep as seen in the three months to October). New orders for goods fell for the 20th consecutive month, and despite easing for the second month in a row, the rate of decline remains large by historical standards, while the loss rate for new orders in the services sector remains at an all-time high It is in. It takes three years to record six consecutive months of decline.

As a result, the backlog also fell significantly, marking the 17th time in the last 18 months and the decline was greater than in November. The manufacturing industry's order backlog continued to decline particularly sharply, while the service sector's order backlog also declined for the sixth consecutive month in December, depleting at the fastest pace since February 2021.

The worrying trend continues to be that new orders, the study's main measure of demand growth, continue to fall faster than production, which is quite unusual by historical standards. This divergence signals continued downside risks to production in the short term unless there is an imminent upward trend in demand growth, and certainly indicates the development of excess capacity.

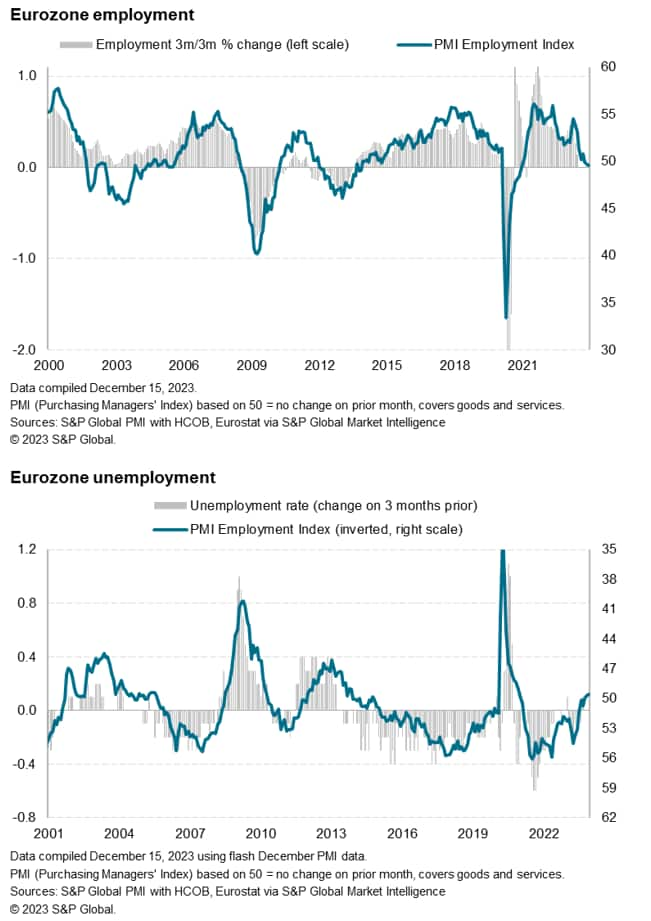

Employment declines for second consecutive month

Employment fell for the second consecutive month as companies cut production capacity in response to a weakening demand environment. Although small, the recent employment decline was the first recorded since early 2021.

PMI data broadly shows stagnant employment in the economy and moderate upward pressure on the unemployment rate.

This is the seventh straight month of manufacturing layoffs, and the job loss rate remains at the highest level since 2012, excluding the months of the pandemic. Meanwhile, service providers continued to cut jobs, resulting in very modest growth in headcount, in contrast to the strong employment growth seen in the sector earlier this year.

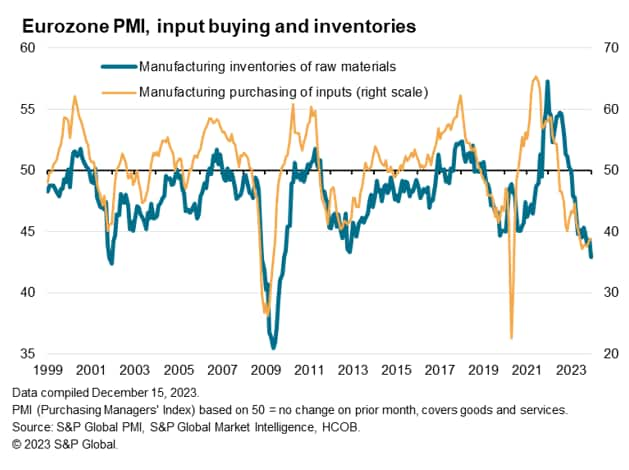

Inventory and purchasing

In addition to job cuts, manufacturers cut purchasing activity at the steepest pace recorded since the global financial crisis, resulting in the largest decline in raw material inventories since November 2009. Inventories of finished goods likewise continued to largely shrink. Responding to cost reduction amidst sluggish sales.

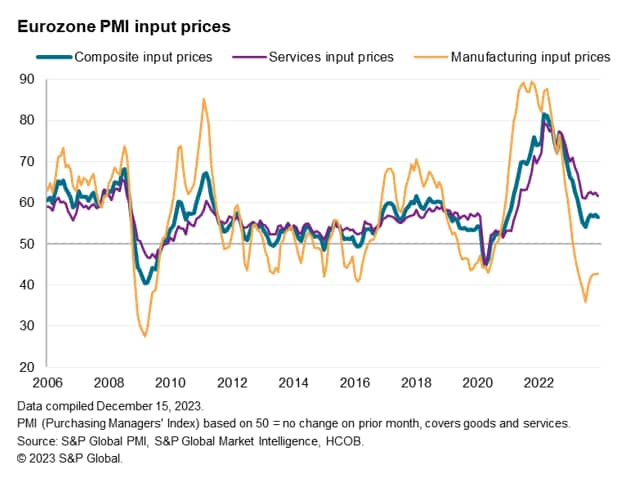

Signs of a stubborn inflation recovery

Eurozone companies recorded a slower rate of increase in input costs, with the smallest monthly increase since August and slightly above the pre-pandemic survey average. Manufacturing input prices fell for the 10th consecutive month, and the rate of decline remained at the highest level since the global financial crisis, while service sector input cost inflation fell further to the lowest level since July. Although it has cooled down, the latter is still going on. High even by historical standards.

While input cost inflation slowed in December, average selling prices picked up the rate of increase, registering the largest monthly increase since May and remaining high by the survey's historical standards. . Commodity prices fell for the eighth consecutive month, but the decline was small and hit the lowest level since May. Meanwhile, service fees rose at the fastest pace since July.

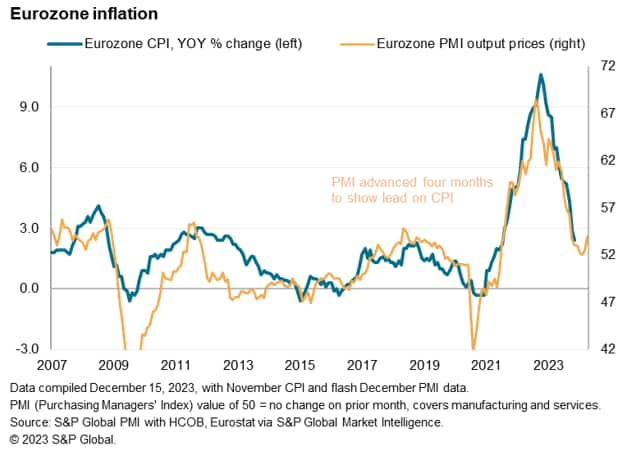

Looking at the inflation inference, the overall signal from the sales price index PMI is that CPI inflation will remain broadly unchanged on average in the coming months, declining slightly from the current 2.4% pace and in line with the ECB's target2. %. It will rise again in early 2024, but will likely remain below 3%.

national trends

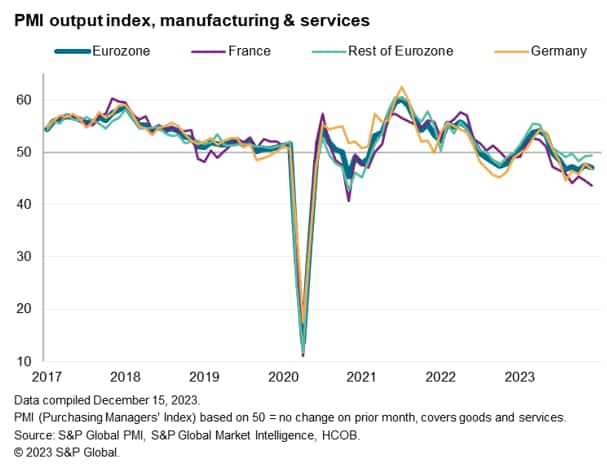

The economic downturn was led by France, where companies reported the sharpest decline in activity (excluding the pandemic) since March 2013, as contraction rates accelerated in both manufacturing and services. However, in Germany too, production fell sharply and at an accelerating rate, amid mounting losses in both goods and services.

Although the rest of the euro area as a whole recorded a more modest decline compared to the declines seen in France and Germany, the continued severe decline in goods production means that euro area output is now at 5. It has been decreasing for consecutive months. service activities.

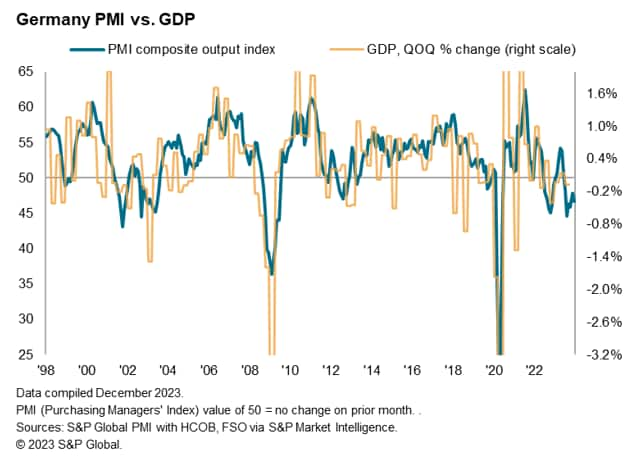

Germany's PMI preliminary data showed GDP fell 0.4% in the fourth quarter compared to the previous quarter, and 0.4% on a December quarter basis.

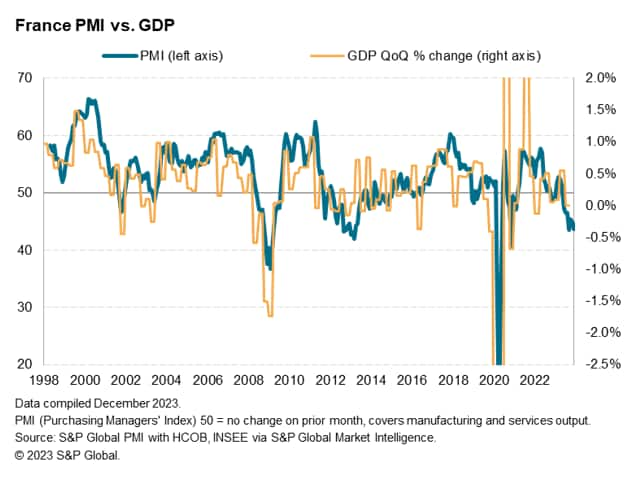

France's PMI preliminary data shows GDP in the fourth quarter fell by 0.2% sequentially, with the December quarterly run rate falling by 0.3%.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Phone: +44 207 260 2329

chris.williamson@spglobal.com

© 2023, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers Index™ (PMI)®) Data is compiled by S&P Global for more than 40 economies around the world. Monthly data comes from a survey of senior executives at private companies and is available by subscription only. The PMI dataset includes headline numbers that indicate the overall health of the economy and sub-indices that provide insight into other key economic factors such as GDP, inflation, exports, capacity utilization, employment, and inventories. Masu. PMI data is used by financial and corporate professionals to better understand where the economy and markets are heading and to uncover opportunities.

Learn more about PMI data

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, an independently managed division of S&P Global.