Image © Adobe Images

The picture is mixed for the eurozone economy in March this year, with manufacturing still in contractionary territory, although the region's services sector continues to recover.

At the same time, regions such as Greece, Spain and Italy continue to outperform the economic powerhouses of Germany and France, highlighting the rise of two-speed economies.

The euro area's services sector has entered further expansion mode, with March's PMI reading at 51.1, beating Farbrey's 50.2 and the consensus estimate of 50.5.

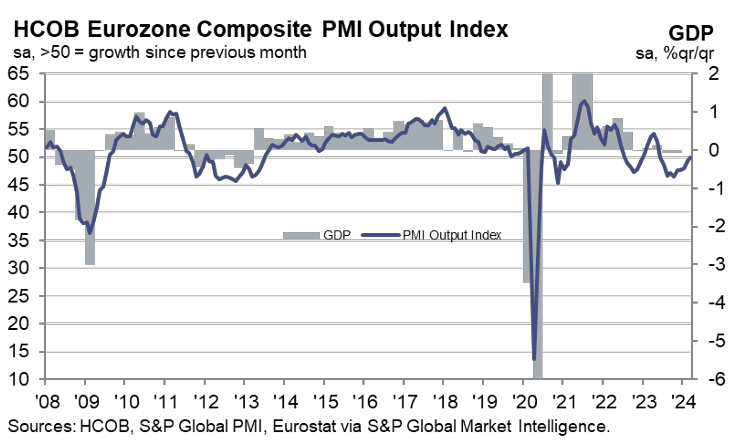

Above: PMIs are consistent with a flattening of the eurozone economy and do not challenge market expectations for an ECB rate cut in June.

However, the manufacturing PMI fell to 45.7 (compared to the index of 47) from 46.5 in February, disappointing. As a result, the overall PMI was 49.9, below the key 50 level that marks the dividing line between growth and contraction. Still, this is higher than February's 49.2 and the expected 49.7.

The overall figures confirm that business activity in the euro area is nearing stabilization this month, according to S&P Global. “The headline PMI rose to 49.9 from 49.2 in March, the highest level since June last year,” said Bart Collin, senior eurozone economist at ING. However, economic stagnation is expected to continue for the time being.”

The PMI figures reaffirm one of the most extraordinary developments of recent times: the disparity in fortunes between the euro zone's core countries, such as Germany and France, and its periphery.

PMI reports that production continues to decline in France and Germany, but is offset by “general improvement” in the rest of the eurozone, which S&P Global says reflects “uneven economic conditions”. It is said to be showing.

Germany is weighed down by its sluggish industrial sector, which has never recovered from the gas price shock caused by Russia's invasion of Ukraine. Germany's manufacturing PMI was 41.6, lower than February's 42.5 and also below expectations of 43.1. Germany's most important sectors remain in deep freeze.

The rest of the eurozone (excluding France and Germany) generally increased output for the third month in a row, with the rate of expansion reaching its highest level in 11 months.

The impact of this report on the European Central Bank (ECB) and, by extension, on the euro exchange rate is likely to be limited. There is nothing to dispute market expectations for a June rate cut.

The slowdown in production in France and Germany hardly equates to significant demand-driven inflation risks that will delay interest rate hikes.

At the same time, the PMI report revealed that input cost and selling price inflation in the services sector remains high compared to historical norms due to rising wage costs. However, a slowdown in the pace of increase in cost burdens was recorded to relieve some of the upward pressure on overall selling prices.