The dollar continues to struggle to find direction, remaining stuck in a familiar range against most major currencies except the Swiss franc. Market focus has now shifted to the soon-to-be-released US PCE data for April as guidance. Currently, Fed funds futures indicate a 50/50 chance of a rate cut by September. Recent comments from Fed officials suggest further rate hikes are unlikely. However, if today's data suggests inflation is accelerating again, the Fed outlook and market sentiment could change dramatically. However, barring any major surprises, attention is likely to shift to next week's employment report.

The euro is currently at its weakest this week amid the release of the eurozone's flash CPI figures. Expectations are for headline CPI to rise slightly to 2.5% and core CPI to stabilize at 2.7%. The ECB is set to implement its first interest rate cut of the cycle next week, but further cuts are unlikely in July as the central bank aims to carefully manage market expectations. Traders are looking beyond today's figures to next week's interest rate decision and future economic forecasts.

Across the market, the Swiss franc remains in the strongest position this week, followed by the yen and the Australian dollar. The euro is in the weakest position, followed by the British pound and the Canadian dollar, while the US dollar and New Zealand dollar are mixed in the middle.

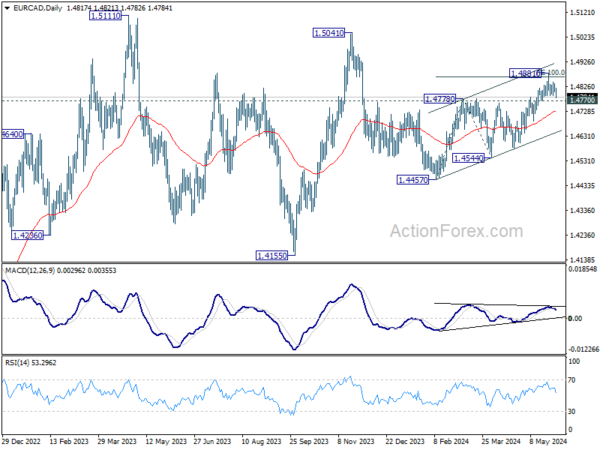

EUR/CAD will be an interesting currency to watch today, given that Canada will release its GDP data. A break above the 1.4770 support would confirm a short-term ceiling at 1.4881. More importantly, in this case, a corrective bounce from 1.4457 could also be completed after reaching the 100% projection from 1.4544 to 1.4457. A further drop to the 55-day EMA (currently 1.4729) is possible. A sustained drop there would increase the likelihood of a resumption of the decline from 1.5041 to 1.4457.

In Asia, at the time of writing, the Nikkei Stock Average was up 1.11%. Hong Kong's HSI was up 1.06%. China's Shanghai SSE was up 0.04%. Singapore's Straits Times was up 0.27%. Japan's 10-year government bond yield was up 1.071, up 0.0115. The Dow was down -0.86% overnight. The S&P 500 was down -0.60%. The Nasdaq was down -1.08%. The 10-year government bond yield was down -0.070 to 4.554.

Fed President Williams: Policy is appropriate, no further rate hikes expected

New York Fed President John Williams told CNBC last night that current monetary policy is “appropriate” and “container” and sufficient to bring inflation down to its target level. He said further rate hikes are unlikely, calling them “not likely.”

Based on his analysis of the data, Williams stressed that U.S. interest rates “will eventually need to be lowered,” but the timing will depend on how effectively the Fed achieves its targets. He expects inflation to ease in the second half of the year as the economy becomes more balanced and global inflationary pressures ease.

But Williams stressed that “inflation remains above our 2 percent longer-run objective and I remain very focused on ensuring we achieve our twin mandate objectives.”

Fed President Bostic: No rate hikes expected, but inflation risks remain

Atlanta Fed President Raphael Bostic told Fox Business last night that he doesn't think further rate hikes are needed to bring inflation down to target, but warned that if inflation rises again, “we have to consider the possibility that rate hikes may be appropriate.”

Bostic stressed that before he supports a rate cut, he would need economic data to show the economy is “robust enough” and inflation is approaching the Fed's 2% target, but clarified that “that's not my outlook today.” He expects inflation to decline “very slowly” over the course of the year, reaching the 2% target sometime after 2025.

Fed's Logan: Interest rates may be looser than expected

Dallas Fed President Rory Logan suggested at an overnight event that interest rates may not be as “tight” as policymakers had expected.

She stressed the need for flexibility, adding: “It's really important that we look at all our options and remain flexible.”

However, Logan also noted there was “good reason” to believe inflation was on its way back up to 2 percent, “perhaps a little slower and a little more choppy than we thought at the beginning of the year.”

Japan's Tokyo core CPI rises in May, industrial production weakens in April

Japan's Tokyo CPI core (excluding fresh food) rose to 1.9% y/y from 1.6% in May, in line with expectations. The increase was mainly due to higher electricity prices. However, CPI core (excluding food and energy) slowed slightly to 1.7% y/y from 1.8%. Private sector services inflation also slowed to 1.4% y/y from 1.6% y/y. Headline CPI rose to 2.2% y/y from 1.8% y/y.

Industrial production in April fell 0.1% from the previous month, falling short of the expected 1.5% increase from the previous month. The Ministry of Economy, Trade and Industry maintained its view of industrial production, saying it “showed weakness amid repeated volatile fluctuations.” Of the 15 industrial sectors surveyed, seven sectors saw declines in production and eight sectors saw increases. Manufacturers expect production to increase 6.9% in May and decline 5.6% in June.

Additionally, retail sales rose 2.4% in April from a year earlier, beating expectations of a 1.9% increase, and the unemployment rate remained steady at 2.6%.

China manufacturing PMI contracts again in May

China's official PMI manufacturing index fell to 49.5 from 50.4 in May, below the expected 50.5 and signaling a contraction after two months of expansion. The new manufacturing export orders sub-index also fell sharply to 47.2 from 50.6 in April, highlighting weakening external demand.

The non-manufacturing PMI index edged down to 51.1 from 51.2, below the expected 51.5. Within the sector, the construction new orders sub-index fell to 44.1 from 45.3, while the services sector business activity sub-index fell to 47.4 from 50.3, indicating a decline in activity.

The composite PMI index, which combines manufacturing and non-manufacturing data, fell to 51.0 from 51.7, indicating a slowdown in overall economic activity.

Looking to the future

The main focus of the European session will be the Eurozone CPI flash. German import prices and retail sales, Swiss retail sales, French consumer spending and UK mortgage approvals will also be released. Later in the day, Canada will release its GDP, while the US will release personal income and spending, PCE inflation and Chicago PMI.

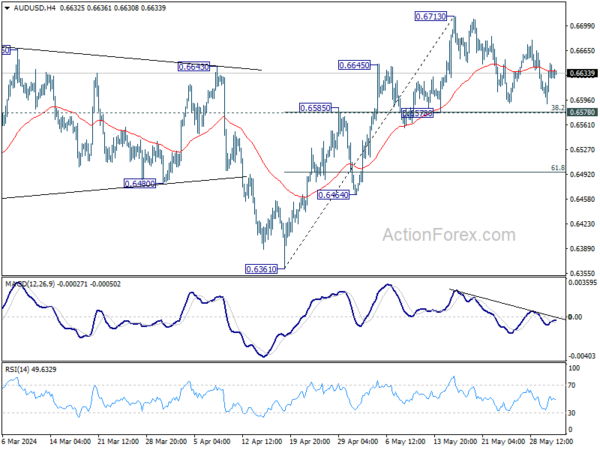

AUD/USD Daily Report

Daily pivots: (S1) 0.6599; (P) 0.6624; (R1) 0.6656; etc…

AUD/USD maintains consolidation from 0.6714 and intraday bias remains neutral. Further upside is expected as the 0.6578 cluster support (0.6579, which is the 38.2% retracement of 0.6361 to 0.6713) holds. On the upside, a solid break of 0.6713 would resume the upside towards the resistance at 0.6361 to 0.6870. However, a sustained break of 0.6578 would weaken this bullish view and result in a deeper drop towards the 61.8% retracement of 0.6495.

In the bigger picture, the price move from 0.6169 (2022 low) is seen as a medium-term correction pattern to the downtrend from 0.8006 (2021 high). The drop from 0.7156 (2023 high) is seen as the second phase, which may have already been completed at 0.6269. The uptrend from there is seen as the third phase, which is currently attempting to resume by breaking through the resistance at 0.6870.

Economic Updates

| GMT | C.C. | event | Actual | forecast | previous | revision |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI YoY May | 2.20% | 1.80% | ||

| 23:30 | JPY | Tokyo CPI Excluding Fresh Foods, Year-on-year Change, May | 1.90% | 1.90% | 1.60% | |

| 23:30 | JPY | Tokyo CPI Excluding Food & Energy YoY Change May | 1.70% | 1.80% | ||

| 23:30 | JPY | Unemployment Rate April | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial production in April compared to previous month | -0.10% | 1.50% | 4.40% | |

| 23:50 | JPY | Retail trade year-on-year change April | 2.40% | 1.90% | 1.20% | 1.10% |

| 01:30 | Australian Dollar | Private Sector Credit m/m April | 0.50% | 0.40% | 0.30% | 0.40% |

| 01:30 | CNY | NBS Manufacturing PMI May | 49.5 | 50.5 | 50.4 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI May | 51.1 | 51.5 | 51.2 | |

| 05:00 | JPY | Housing starts YoY April | 13.9% | -0.20% | -12.80% | |

| 06:00 | EUR | German Import Price Index m/m April | 0.50% | 0.40% | ||

| 06:00 | EUR | German Retail Sales Month-on-Month April | 0.10% | 1.80% | ||

| 06:30 | Swiss franc | Real retail sales YoY April | 0.20% | -0.10% | ||

| 06:45 | EUR | French GDP QoQ 1 | 0.20% | 0.20% | ||

| 08:30 | GBP | Mortgage Approvals April | 62K | 61K | ||

| 08:30 | GBP | M4 Money Supply Monthly Change April | 0.40% | 0.70% | ||

| 09:00 | EUR | Eurozone CPI YoY May | 2.50% | 2.40% | ||

| 09:00 | EUR | Eurozone CPI Core YoY Change May | 2.70% | 2.70% | ||

| 12:30 | CAD | GDP Monthly Change March | 0.00% | 0.20% | ||

| 12:30 | USD | Personal income change from previous month April | 0.30% | 0.50% | ||

| 12:30 | USD | Personal Expenses April | 0.30% | 0.80% | ||

| 12:30 | USD | PCE Price Index m/m April | 0.30% | 0.30% | ||

| 12:30 | USD | PCE Price Index YoY April | 2.70% | 2.70% | ||

| 12:30 | USD | Core PCE Price Index m/m April | 0.30% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index YoY April | 2.80% | 2.80% | ||

| 13:45 | USD | Chicago PMI May | 40 | 37.9 |