Preliminary data from the PMI® survey showed business activity in the euro area fell by the lowest in eight months in February, as stabilizing production in the services sector offset a further sharp decline in manufacturing. Business confidence for next year improved, reaching a 10-month high, prompting companies to raise staffing levels at the fastest pace since July last year and increasing signs that the euro zone's economic slump is easing.

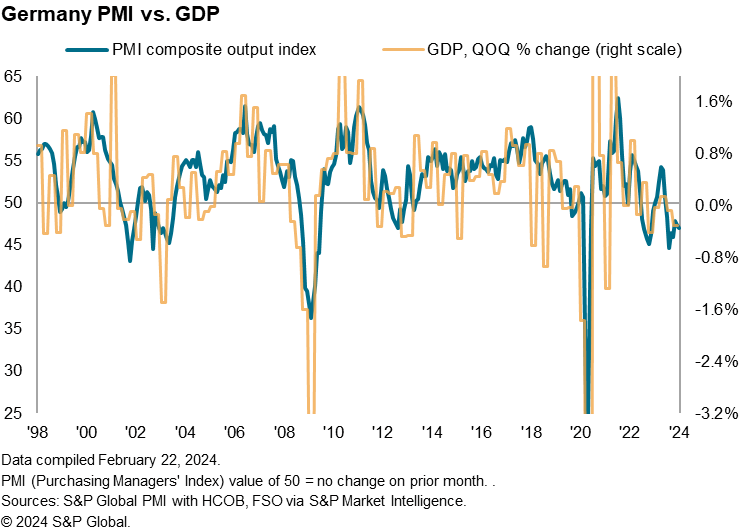

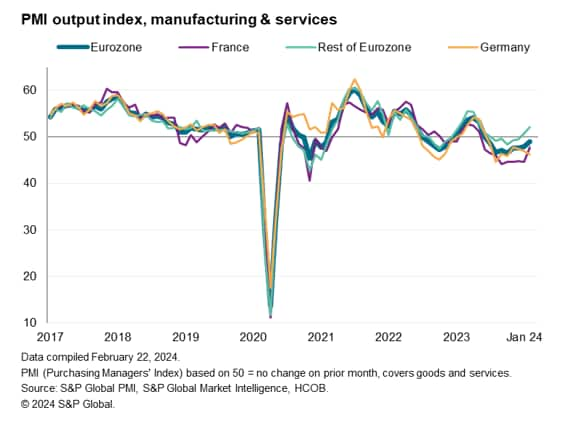

On a country-by-country basis, a deepening economic slowdown in Germany and a sustained decline in production in France were offset by faster growth in other regions.

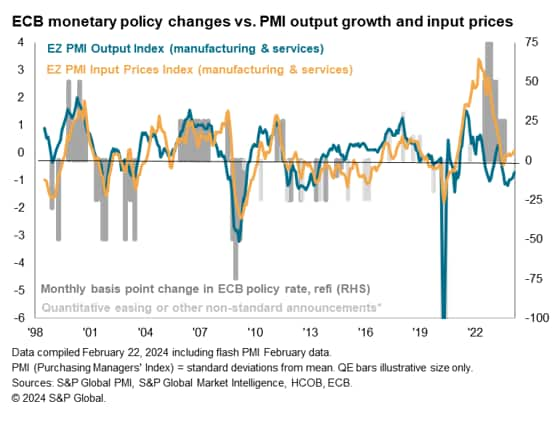

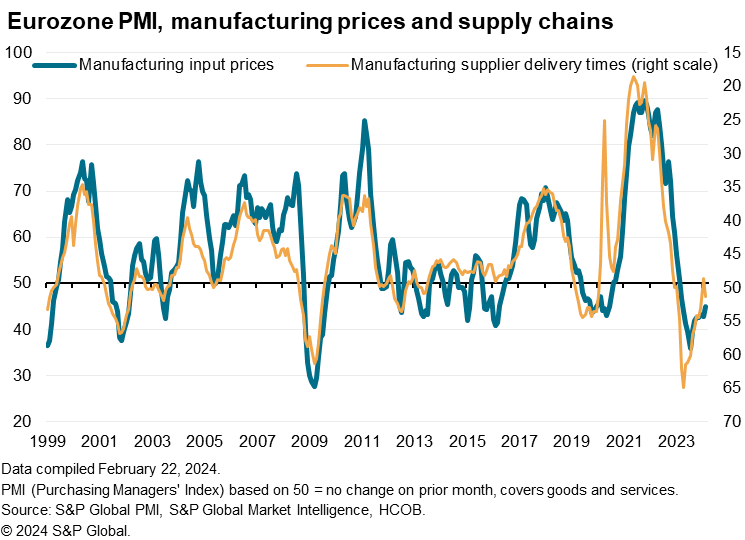

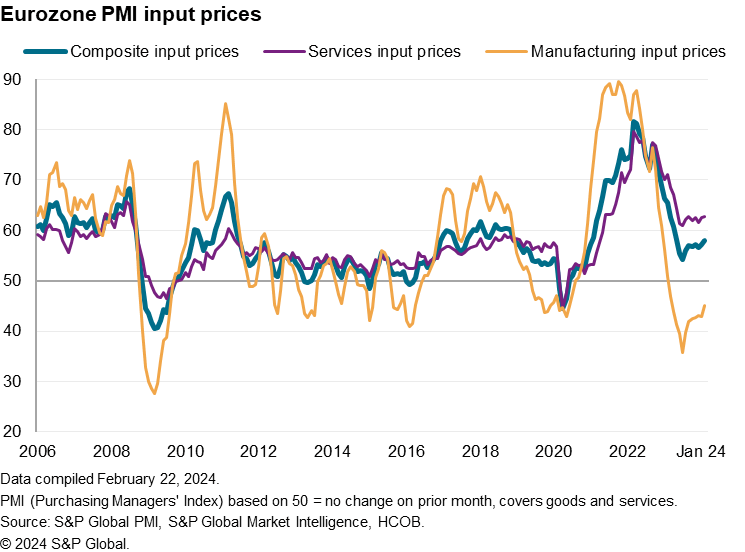

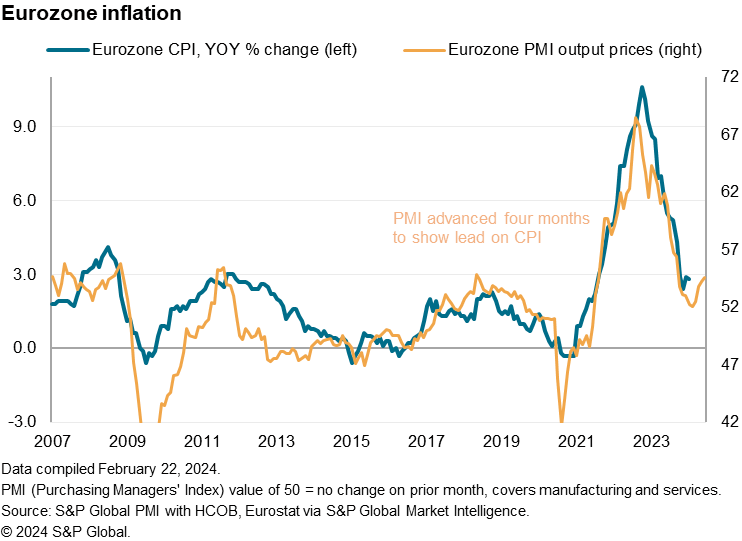

Supplier delivery times have improved, relieving further pressure on manufacturing prices, after delays seen in January due to Red Sea shipping disruptions. However, service sector inflation remains high compared to historical standards, with input cost inflation and overall sales price inflation accelerating in February to their highest levels since May last year.

Eurozone economic slump subsides

The seasonally adjusted HCOB Flash Eurozone Composite PMI Production Index, compiled by S&P Global based on about 85% of regular survey responses, rose to 48.9 in February from 47.9 in January. Although this marks the ninth consecutive month of production decline, February's decline was the smallest since June of last year.

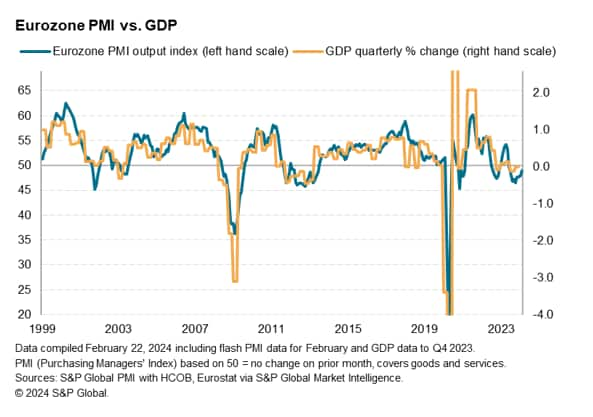

Latest findings suggest the eurozone's deepest contraction since 2013 (excluding the early months of the pandemic) continues into 2024, but the rate of decline in the first quarter shows signs of easing. is showing. Eurozone GDP contracted at a quarterly rate of 0.15%, after falling 0.25% in the fourth quarter, according to the first quarter PMI data available so far.

The latest provisional GDP figures estimate that the eurozone economy stagnated in the fourth quarter, with PMIs suggesting that this figure will eventually be revised downward.

However, business conditions continue to vary markedly across sectors and countries across the euro area, highlighting weakness in manufacturing in particular, which has hit Germany particularly hard.

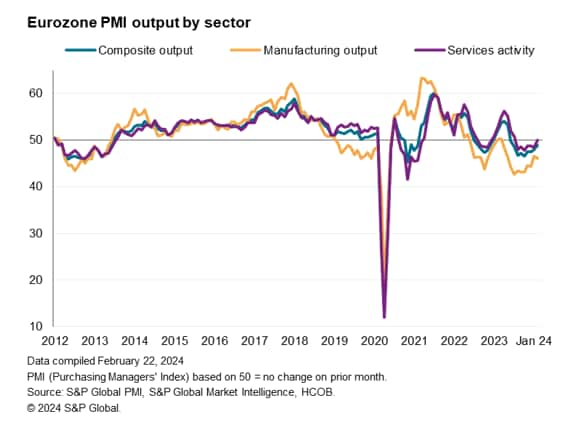

Manufacturing industry stagnates, services remain stable

Manufacturing production fell for the 11th straight month across the euro area in February, marking another month of sharp contraction, accelerating again from the slow decline seen in January. New orders for products similarly declined significantly compared to historical norms (although loss rates slowed slightly for the fourth consecutive month). In contrast, business activity in the services sector stabilized in February after six consecutive months of deterioration, as the rate of decline in new business eased for the fourth consecutive month, with only a slight decline in demand. It shows.

german drugs

By country, Germany's production declined particularly sharply, declining for eight consecutive months at the fastest pace since October last year. A mild downturn in Germany's services sector has only partially offset the deepening contraction in manufacturing.

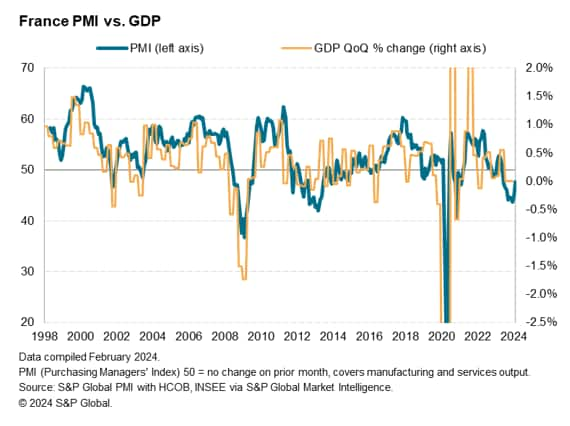

Production also contracted in France, but the decline was the smallest since France's economic downturn began in June last year, as the pace of deterioration in both manufacturing and service sector output slowed.

Meanwhile, other countries in the euro area reported a second consecutive month of production growth, in contrast to declines over the previous five months, enjoying the biggest monthly improvement since May last year. As growth in the services sector accelerated, manufacturing output also remained more or less stable.

employment

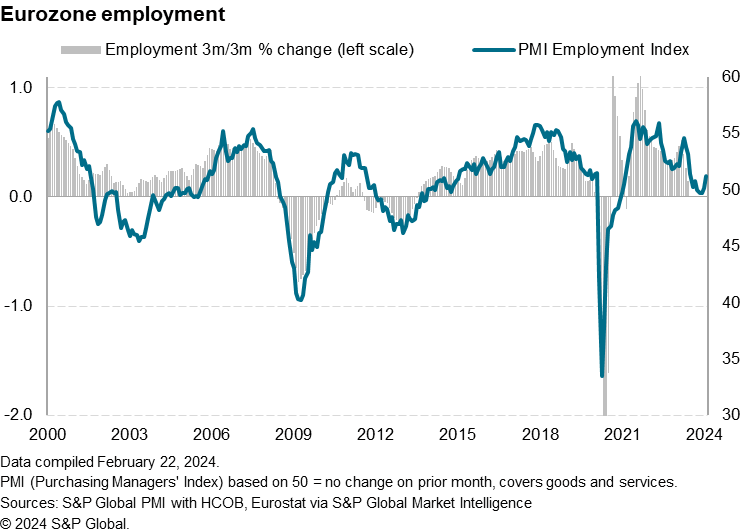

Employment increased for the second consecutive month in February after declining for two months at the end of 2023. While overall employment growth was only modest, the latest increase was still the largest since July of last year.

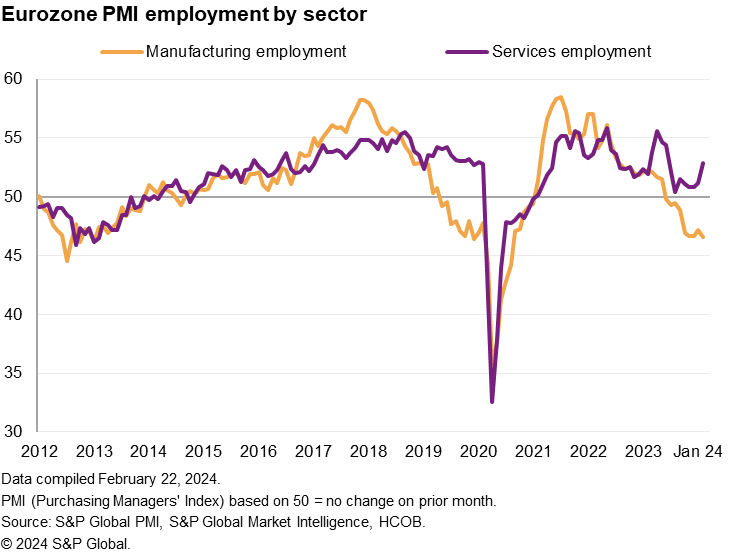

Again, sector differences were notable. In contrast to the sharp rise in manufacturing job losses, net employment in services rose to an eight-month high. Employment fell slightly in Germany, but rose slightly in France, and job creation rates in other regions rose to the highest level in nine months.

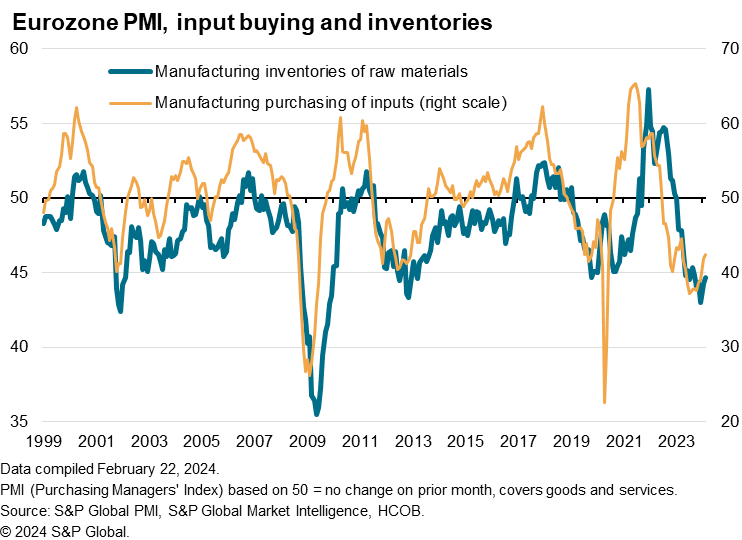

Inventory, supply chain, purchasing

The gloom in the manufacturing sector is further accentuated by the continued sharp decline in raw material purchases by factories, which have now declined for 20 consecutive months, and as a result, inventories of purchased goods have also declined for 13 consecutive months. is decreasing.

Encouragingly, continued reductions in raw material purchases have eased pressure on the supply chain. In January, supplier delivery times extended for the first time in 12 months, largely due to Red Sea-related transport disruptions, but February saw a welcome improvement in lead time reductions, reducing shipment delays. There were signs that it should.

Price pressure will increase further

Growth in average input costs across producers of goods and providers of services accelerated for the second month in a row, reaching the highest level since May last year. While well below the highs seen during the pandemic, recent increases are still higher than the survey's long-term pre-pandemic average, indicating increasing cost pressures by historical standards. Input cost inflation in the services sector rose to its highest level in nine months, while price declines in manufacturing fell to its lowest level in 11 months.

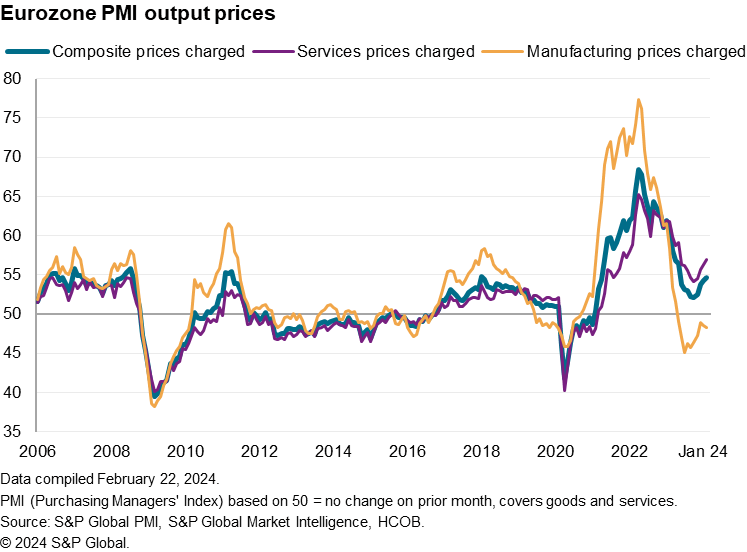

Sales price inflation accelerated as well, rising for the fourth straight month in February and hitting its highest level since May last year. Excluding price increases seen in the two years to last May, inflation in February was the highest since January 2018 and well above the long-term average in pre-pandemic surveys.

Prices charged by manufacturers fell at a slightly higher rate, continuing the disinflationary trend seen in goods over the past 10 months, while prices charged for services rose at the steepest rate for nine months. Inflation accelerated for the fourth consecutive month. Excluding the 19 months ending in May last year, the recent increase in prices in the service sector was the largest since September 2000.

Comparing PMI sales price data and consumer price inflation, the latest survey data is consistent with the CPI sticking to some extent around 3% in the short term, indicating some difficulty in achieving the ECB's 2% target. This suggests that it is difficult. At least in the first half of 2024.

Outlook

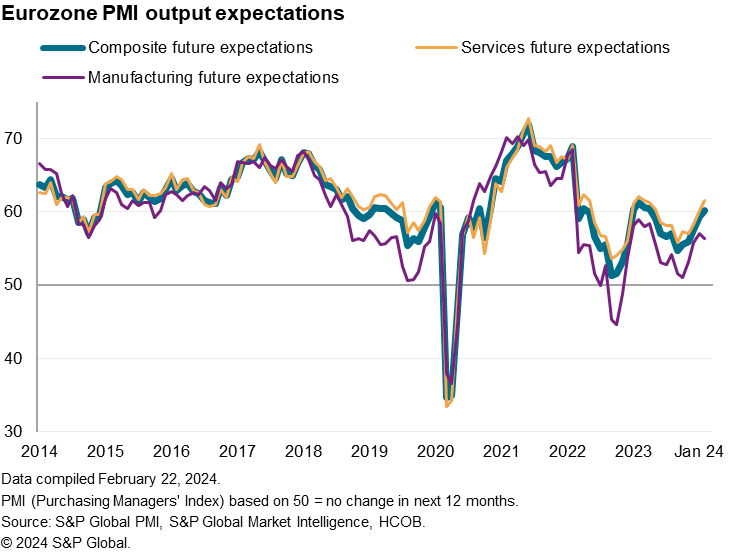

Looking ahead, business optimism for the next 12 months improved for the fifth consecutive month in February, rising to its highest level since April last year. Confidence in the services sector improved to an 11-month high, further recovering from its lowest level in September last year. However, manufacturing sentiment has fallen slightly from a nine-month high in January, although it remains well above the lowest level recorded in October last year.

Growth prospects have improved in recent months on hopes of easing cost-of-living pressures, lower interest rates next year, and signs that manufacturing inventory reduction policies are winding down. Nevertheless, the outlook for the year ahead remains slightly below the pre-pandemic average, due in part to economic uncertainty and global geopolitical concerns.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Phone: +44 207 260 2329

chris.williamson@spglobal.com

Purchasing Managers Index™ (PMI)®) Data is compiled by S&P Global for more than 40 economies around the world. Monthly data comes from a survey of senior executives at private companies and is available by subscription only. The PMI dataset includes headline numbers that indicate the overall health of the economy and sub-indices that provide insight into other key economic factors such as GDP, inflation, exports, capacity utilization, employment, and inventories. Masu. PMI data is used by financial and corporate professionals to better understand where the economy and markets are heading and to uncover opportunities.

Learn more about PMI data

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, an independently managed division of S&P Global.