Asian financial markets today are showing significant divergence. Japan's Nikkei Stock Average reacted sharply to the ruling Liberal Democratic Party's election results from last Friday, plunging by more than -4%. Shigeru Ishiba, the newly elected Liberal Democratic Party leader and Japan's next prime minister, sought to soften his previously hawkish stance on Bank of Japan monetary policy in an interview on Sunday. Despite these efforts, investors remain concerned about the impact of further monetary tightening on the Japanese yen's strength and the subsequent impact on the export-driven economy.

In stark contrast, stock markets in Hong Kong and mainland China have continued their strong gains, supported by the stimulus measures implemented last week. Markets have largely ignored China's disappointing PMI data released today. However, pressure is growing for additional fiscal policy to supplement monetary efforts. Proposals include expanding the government's balance sheet to stimulate consumer spending and strengthen social welfare programs. China's economy continues to face challenges from weak domestic demand and a deteriorating global trade environment.

Turning to currency markets, the Kiwis and Australia are leading the gains as the new week begins. Kiwis are doing particularly well, backed by extremely positive business confidence data. The pound is also doing well, ranking as the third strongest currency as of today. The yen, on the other hand, is the worst performer, but this appears to be just a consolidation following last week's rally, and is expected to rise further in the future. The Swiss franc and dollar are also weak, but the euro and loonie are in the middle.

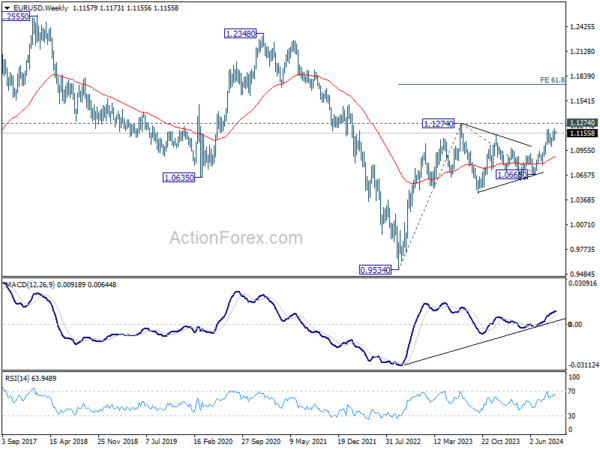

Looking ahead, EUR/USD will be the main focus this week, with Eurozone inflation data and US non-farm payrolls important in shaping the ECB and Fed's next policy decisions.

Technically, EUR/USD has struggled so far to build upward momentum above the resistance at 1.1274 (2023 high). However, a significant break above this level would confirm the resumption of the overall uptrend from 0.9534 (2022 low). This sets the stage for a further rally towards a 61.8% forecast of 0.9534 to 1.1274 from 1.0665 of 1.1740 in the fourth quarter by the end of the year.

In Asia, the Nikkei Stock Average is down -4.56% at the time of writing. Hong Kong HSI rose 3.01%. China's Shanghai SSE rose 5.70%. Singapore's Strait Times rose 0.20%. Japan's 10-year government bond yield rose 0.0551 to 0.862.

Japan's industrial production decreased by 3.3% in August compared to the previous month, with recovery expected in the coming months

Japan's industrial production took a big hit in August, falling -3.3% month-on-month, significantly missing market expectations for a -0.5% month-on-month decline.

The seasonally adjusted production index for factories and mines was 99.7, based on the 2020 benchmark of 100. Out of the 15 industrial sectors covered by the survey, production decreased in 12 sectors, with automobiles in particular leading the way with a -10.6% month-on-month decline. The main reason for this decline was the suspension of operations at more than a dozen Toyota Motor plants due to Typhoon Shanshan.

Despite this significant decline, Japan's Ministry of Economy, Trade and Industry maintained its judgment that industrial production remains “unpredictable.” Manufacturers surveyed by the ministry are forecasting a recovery, with production expected to increase by 2.0% month-on-month in September and a further 6.1% month-on-month increase in October.

On a positive note, Japan's retail sales rose 2.8% year-on-year in August, beating the median estimate of 2.6% year-on-year growth. Compared to the previous month, retail sales increased 0.8% month-on-month, following a 0.2% month-on-month increase in July, indicating solid consumer demand.

China's PMI data suggests continued contraction in manufacturing and weakening of services sector

China's economic indicators in September painted a mixed picture, with manufacturing continuing to contract and the services sector losing momentum.

NBS's official manufacturing PMI rose slightly to 49.7 from 49.1 in August, beating expectations of 49.5 but still below the 50 milestone, suggesting a fifth consecutive month of contraction. Export orders continued to be weak, with the new manufacturing export orders sub-index falling from 48.7 to 47.5.

Meanwhile, the NBS non-manufacturing PMI fell from 50.3 to 50.0, ending 20 consecutive months of expansion. Among non-manufacturing industries, the construction industry showed a slight improvement, with the sub-index rising to 50.7, but the service industry fell from 50.2 to 49.9, falling into contraction territory.

The NBS PMI composite rose slightly from 50.1 to 50.4. According to NBS, extreme weather events such as typhoons and the end of the summer travel season have had a major impact on the transportation, culture and entertainment sectors.

Caixin Manufacturing PMI showed similar results, dropping from 50.4 to 49.3, its lowest reading since July 2023, while Caixin Services PMI also fell from 51.6 to 50.3, its lowest in 12 months. It became the standard. Caixin's composite PMI fell to 50.3 from 51.2, reflecting broader weakness in both manufacturing and services.

Wang Zhe, senior economist at Caixin Insight Group, said, “Manufacturing market conditions worsened in September, characterized by limited supply expansion and significant demand contraction.” Business confidence also fell to the “lowest level in recent years.''

NZ ANZ business confidence soars to 60.9, raising concerns about overreaction to RBNZ rate cut

New Zealand's ANZ Business Confidence Index rose significantly in September, jumping from 50.6 to 60.9, reflecting growing optimism in the business sector.

Key elements of the study also made a positive impression. Own activity outlook rose from 37.1 to 45.3, and earnings expectations also rose from 8.0 to 22.2, suggesting a brighter economic environment.

Cost expectations fell slightly from 68.3 to 66.8, while wage expectations rose slightly from 75.1 to 76.4. Pricing intentions also rose from 41.0 to 42.8, while inflation expectations remained unchanged at 2.92%, staying below 3% for the second consecutive month.

ANZ said the survey highlighted “the risk that the economy's response to lower interest rates will be more vigorous than generally expected.”

Concerns about inflation remain. Companies plan to raise prices by an average of 1.6% over the next three months, a sharp increase from June's low of 1.2%. Wage growth has slowed to 3% now from 4% in April, and cost expectations have fallen to 2.4%, but the RBNZ still needs to closely monitor inflationary pressures to ensure price stability. .

US NFP and Eurozone CPI will influence future decisions of the Fed and ECB

Next week will see the release of a series of key economic indicators that will shape monetary policy decisions by some major central banks.

in usThe biggest question is whether the Fed will proceed with a consecutive 50 bps rate cut on November 1st. Federal funds futures currently reflect a 53.3% probability of such a move, indicating that the market is evenly divided on the outcome.

As the Fed continues to make good progress in its efforts to curb inflation, it has made clear that it needs to focus more on the other half of its dual mandate: the labor market. The September non-farm employment report, to be released this Friday, will therefore be the most important. Among labor statistics, major employment growth and the unemployment rate are expected to be the factors most influential in the Fed's decision-making process. Wage growth, while still important, may be less emphasized given the current situation.

In addition to employment statistics, the ISM is expected to release indicators for the manufacturing and service industries, which will attract attention. An unexpected deterioration in the services sector could undermine the current bullish momentum in the stock market and reignite recession fears.

in euro areamarket sentiment has shifted sharply in favor of a 25bps rate cut by the ECB on October 17th, with probability estimates jumping from 25% to 75% following the disastrous PMI results. ECB officials have pointed to a lack of up-to-date economic data, but the expected September release of both headline and core CPI offers new insights that could sway decisions. may be provided.

in Japannew Liberal Democratic Party leader Shigeru Ishiba appears to be weakening support for an impending Bank of Japan rate hike. Over the weekend, he reiterated the need for continued monetary easing, citing continued concerns about deflation. For this reason, the market may look to the Bank of Japan's opinion summary and Tankan survey for further guidance. The Bank of Japan remains divided over the timing of future interest rate hikes, and this division is likely to persist in the coming weeks.

Ishiba's position suggests that markets may need to readjust their expectations about the Bank of Japan's policy moves. The focus will likely return to the Tankan survey, which will serve as a summary of the Bank of Japan's opinions and guidelines going forward.

In other places, Switzerland The CPI could confirm that the Swiss central bank is on course for another rate cut in December.

This week's highlights include:

- Monday: Japan's industrial production, retail sales, and housing starts. Business sentiment in New Zealand ANZ. German import prices, CPI news. UK Q2 GDP finalization, current account balance, M4 monthly supply, mortgage approvals. Switzerland's KOF economic barometer. Chicago PMI, USA.

- Tuesday: New Zealand building permits. Japan's unemployment rate, Tankan survey, finalized manufacturing PMI, and summary of the Bank of Japan's opinions. Australian retail sales, building approvals. Swiss retail sales, PMI manufacturing industry. Euro area PMI manufacturing industry final value, CPI preliminary report. UK PMI Manufacturing Final Results. PMI manufacturing industry in Canada. US ISM Manufacturing and Construction Expenditures.

- Wednesday: Japan's monetary base, consumer confidence. Eurozone unemployment rate. ADP employment in the United States.

- Thursday: Australia's trade balance. Swiss CPI. Eurozone PMI Service Final Value, PPI. Final version of the UK PMI service. U.S. unemployment claims, ISM services, and factory orders.

- Friday: Swiss unemployment rate. French industrial production. British PMI construction. US non-farm payrolls. Canadian Ivy PMI.

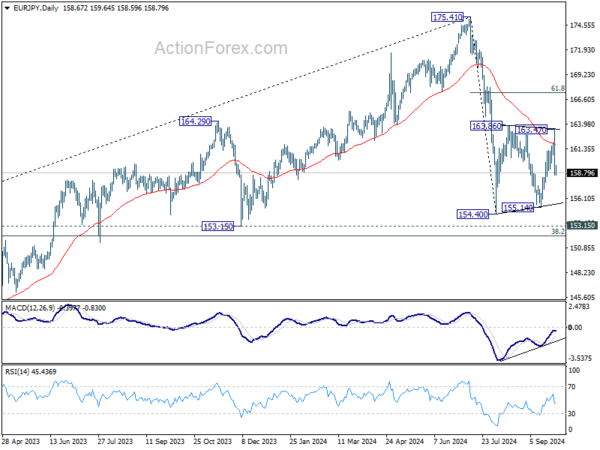

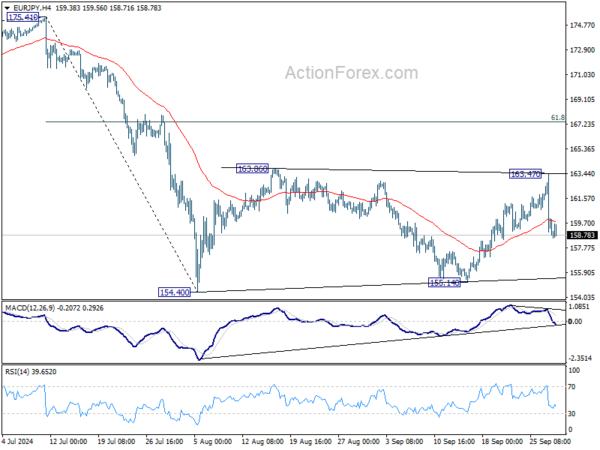

EUR/JPY daily outlook

Daily Pivot: (S1) 157.07; (P) 160.28; (R1) 161.99;More….

The intraday bias for EUR/JPY is currently on a downward trend. Current developments suggest that the corrective pattern from 154.40 may already be completed in three waves to 163.47. A retest of the 154.40/155.14 support zone will likely lead to an even deeper decline. For now, risks remain on the modest downside as long as the resistance at 163.47 holds in case of a recovery.

Looking at the bigger picture, the price movement from 175.41 can be seen as a correction towards an increase from 114.42 (2020 low). The consolidation range should have been set between 114.42 at 152.11 and the 38.2% retracement at 175.41 and the high at 175.41. However, a decisive break at 152.11 would argue that a deeper correction is underway.