: Signs of Bitcoin euphoria peaking")

Coinbase Global (Nasdaq: Coin) is a company that makes the majority of its revenue from consumers trading cryptocurrencies on its platform. However, the company is looking to expand into other crypto spaces, such as crypto storage. I'm bearish on Coinbase because its profits are tied to Bitcoin (BTC-USD) Price appears to be on the uptick, indicating a peak in trading volume. Additionally, the company's business model has so far been questionable, with it being funded through debt, stock dilution, and rising Bitcoin prices.

Why cryptocurrency trading volume has reached its peak

I believe that cryptocurrencies are speculative assets that may wane in popularity over time. For the past few months, every time I've talked to someone about investing, they've asked me if I want to trade Bitcoin. The alternative Crypto Fear/Greed Index, which measures crypto sentiment based on six different factors, hit a near all-time high greed rating in March of this year.

Bitcoin seems to have captured people's imagination because people love getting rich quick. In 2021, everyone was talking about meme stocks and their dog was talking about meme stocks. In retrospect, this marked the peak of the euphoria for these stocks. The same thing happened with the silver commodity in 2011, and fads inevitably die.

Bitcoin has other uses, such as hedging against fiat devaluations and behind-the-scenes (sometimes illegal) trading, but I think people primarily use it for gambling and speculation. To the detriment of other uses of cryptocurrencies, there has been no devaluation of the US currency in the past two years, as evidenced by the US M2 money supply, and illegal activities have put cryptocurrencies at risk of banning.

Bitcoin doesn't work well, even as a currency, because there are very few items that can be purchased with Bitcoin, and the value fluctuates wildly.

Because of this excitement and outlook, I think demand for Bitcoin and other cryptocurrencies is nearing its peak again, which would be bad news for Coinbase. The company's revenue is roughly tied to the price of Bitcoin, and although it reported record profits in 2021 and huge losses in 2022, its revenue has soared again in 2024. Rising prices attract traders and falling prices scare traders. Another problem is that Coinbase holds its own “crypto assets held for investment purposes,” which could magnify losses.

The business model has some flaws

Despite Coinbase's market capitalization of $53 billion, its average operating profit over the past three years has been just $68 million, meaning its core business is not very profitable. Because Coinbase has to protect all of its customers' cryptocurrencies and cash, it has relatively little capital available for investment, making it a fairly unprofitable business.

In response to several flawed business models, Coinbase has increased long-term debt and diluted its shareholders. This has helped Coinbase bring in cash over the past few years.

The company currently owns BlackRock (New York Stock Exchange:BLK). However, since the fees are very low at 0.1%-0.2%, we expect the earning opportunity here to be in the millions instead of billions. Additionally, because consumers have the option to invest in Bitcoin ETFs with minimal fees, we expect this new revenue to only replace lost trading revenue and result in little growth. Masu. Coinbase's transaction fees may also come under downward pressure.

Valuation is a good reason to be bearish

Despite not even discussing the issues outlined above or the ongoing SEC litigation among other risks, Coinbase trades at 13.5 times sales and 6.4 times book value. Comparing this to the company's growth, the company's book value per share has grown at a compound annual growth rate of just 3.5% since 2021, and its revenue has halved since then.

I like to look for companies that are clearly undervalued and, as Peter Lynch once said, “avoid long shots.” Coinbase seems like a long-term goal to me. That doesn't mean it can't grow to that valuation, but looking at all the information available, I'm skeptical.

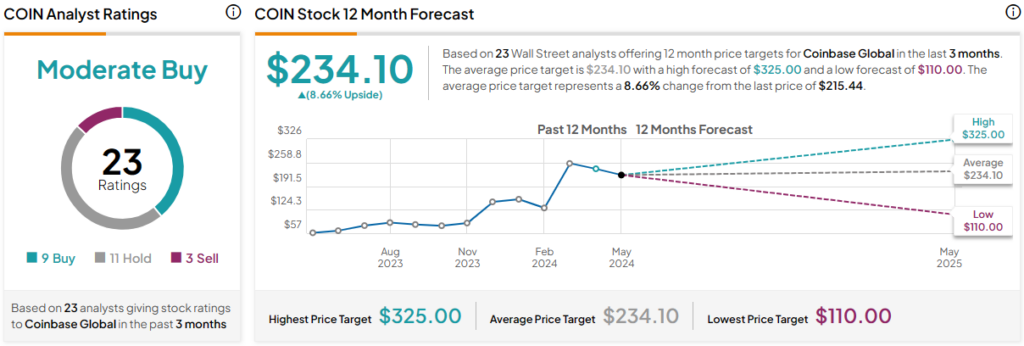

Is COIN stock a buy, according to analysts?

Currently, 9 out of 23 analysts covering COIN have given it a Buy rating, making the consensus rating a Moderate Buy. Coinbase Global's average price target is $234.10, suggesting an 8.7% upside potential. Analyst price targets are as low as $110 per share and as high as $325 per share.

Final result of COIN stock

Coinbase's stock price is similar to what Peter Lynch calls a “long shot.” The $53 billion valuation is quite high for a company that has only generated an average operating profit of $68 million over the past few years. I'm also bearish on Bitcoin. We believe Bitcoin is nearing the peak of its euphoria and could either become a fad of the past or face further bans from governments. With the ongoing SEC litigation and increased competition from Bitcoin ETFs, I think COIN stock has the potential for further decline.

disclosure