Will the Fed further jeopardize its rate cut expectations?

Next week looks sure to be an action-packed week for the US dollar. Besides the FOMC meeting and the April jobs report, there is a flurry of data coming out on the US agenda that will give traders no time to rest.

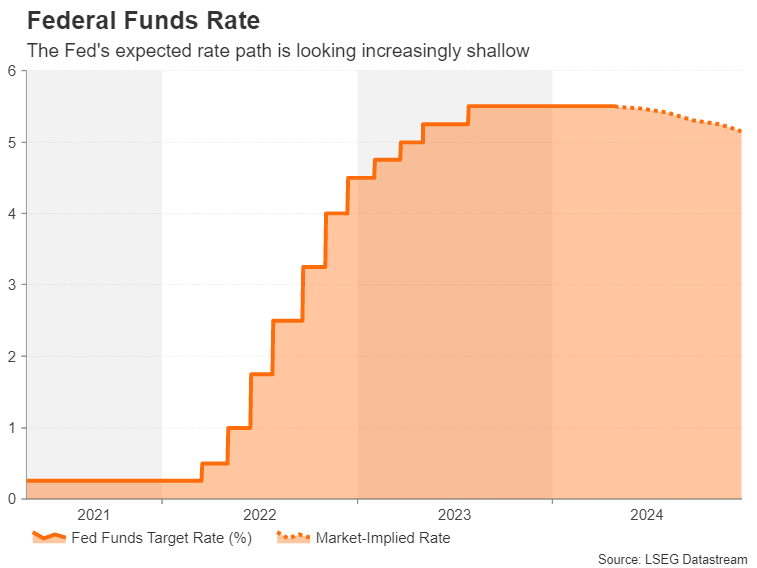

The main focus for the first half of the week will be the US Federal Reserve's policy decision on Wednesday. It wasn't that long ago that the May meeting was seen as the one where policymakers would chart a path to a June rate cut. However, a series of better-than-expected inflation and employment data has pushed the timing of a rate cut further down the line, making it unlikely to happen before September.

The latest FOMC forecast for the May decision has not been released, so investors will be watching every word Powell says at the press conference for clues about how soon the Fed will begin easing policy. There will be. Those holding on to hope that a summer rate cut is still possible will likely be disappointed.

The latest comments from Fed officials suggest that committee members are comfortable remaining dormant for some time, although the majority still expects some easing to occur by the end of the year. are doing. Chairman Powell is likely to reiterate the need for patience, but will likely signal that rate cuts remain.

But what investors are trying to gauge is how confident Powell is that inflation will fall so much in the coming months that policy makers will be less restrictive. If Chairman Powell strikes a slightly more hawkish tone than his usual more balanced approach, the dollar could resume its uptrend.

A labor market that never cools down

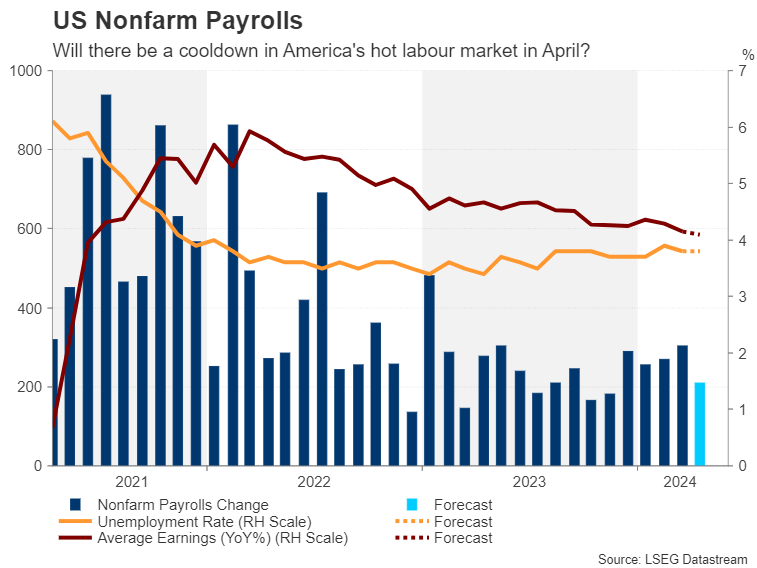

If there is no new signal from the Fed, investors will focus on Friday's nonfarm jobs report. Far from slowing, the US economy added a staggering 303,000 jobs in March. Analysts expect the April figure to be closer to 210,000, but the unemployment rate is expected to remain at 3.8%.

The important factor here is whether the wage increase rate will remain moderate and continue to grow at just over 4.0%. Any acceleration in average hourly wages could spark more panic over the downside of bets on interest rate cuts than over expectations of upside in headline pay statistics.

Investors' focus next week will be on the April ISM Manufacturing PMI and Non-Manufacturing PMI, which will be released on Wednesday and Friday respectively. Following the weaker-than-expected S&P Global Services PMI, a similarly weak ISM Services PMI could potentially offset the impact of strong employment data and a hawkish Fed.

Other announcements on Tuesday will focus on quarterly employment costs, along with Chicago PMI and consumer confidence. Further labor market indicators will be released on Wednesday, consisting of the JOLTS job openings and ADP employment surveys.

Euro eyes GDP and CPI updates as June interest rate cut approaches

A rate cut in June appears to be agreed, pending a surprisingly positive wage report from the ECB at the end of May. What is less certain is the subsequent rate path. The market's year-end forecast has fallen by 75 basis points (roughly three rate cuts) in recent weeks, and Joachim Nagel, the influential head of Germany's Bundesbank, has warned that the June rate cut will not necessarily be followed by a series of further rate cuts. I warned him that it was not necessary.

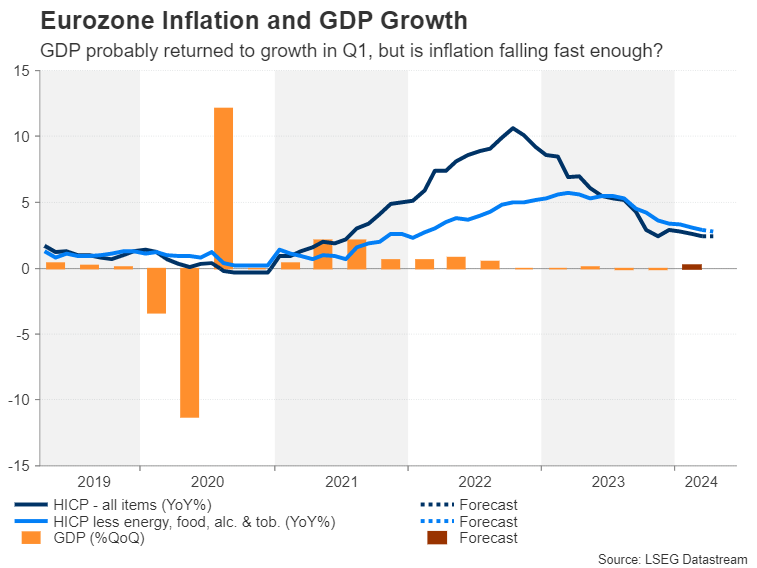

Preliminary first-quarter GDP and April CPI numbers released on Tuesday are likely to further shape expectations for the remainder of 2024, but barring major deviations from expectations, June It is unlikely that the probability will change significantly.

The euro zone economy is likely to expand by 0.2% sequentially in the first three months of this year, after flat growth in the fourth quarter. As the economic outlook improves, there will be less urgency for the European Central Bank to cut interest rates aggressively, so policymakers will need to see inflation fall further to maintain a dovish stance. Headline inflation is expected to remain unchanged at 2.4% in March.

The euro is currently trying to gain a foothold above the $1.07 handle. Success depends on which direction the incoming data goes.

China's PMI and New Zealand's employment are also on the rise

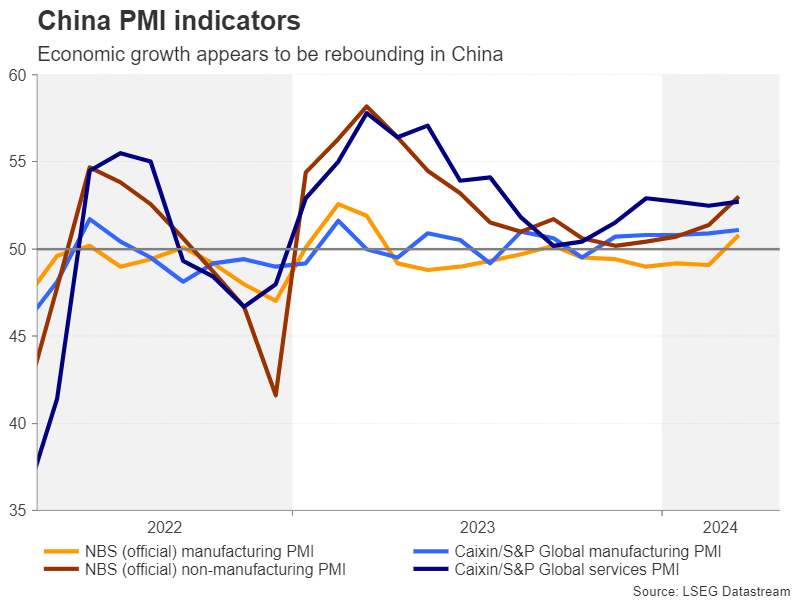

Another region enjoying a rebound in economic activity is China. The official composite PMI rose in March to its highest level since May 2023, but the majority of that was driven by the services sector, with the recovery in manufacturing remaining slow.

The latest PMI readings from both the government and Caixin/S&P Global will be released on Tuesday.

If the economy gains further momentum in April, it would bode well for risk-sensitive assets such as stocks and oil, as well as commodity currencies such as the Australian and New Zealand dollars.

In New Zealand, the local dollar is also keeping an eye on domestic payrolls numbers scheduled for Wednesday. First-quarter data on job growth, unemployment and wages will weigh on how quickly the RBNZ will cut interest rates after the central bank recently gave its strongest indication yet that its next policy cut would be It may be a clue about.

It could come under pressure if the labor market appears to be slowing.

Elsewhere, Canada will release its monthly GDP estimates on Tuesday, and Japan will release preliminary industrial production figures for March on the same day. Switzerland will release its April CPI data on Thursday, and the Norwegian Central Bank will announce its decision on interest rates on Friday.

remove ads

.